.png)

Mega-cap tech companies led the market higher in 2025, fuelled by significant capital expenditures—reportedly over $1.2 trillion by S&P 500 companies.1 Nvidia became the first company to reach a $5 trillion market capitalization—worth more than the GDP of every country except the U.S. and China, according to World Bank data. This has prompted many to ask: “Can AI deliver on its potential?”

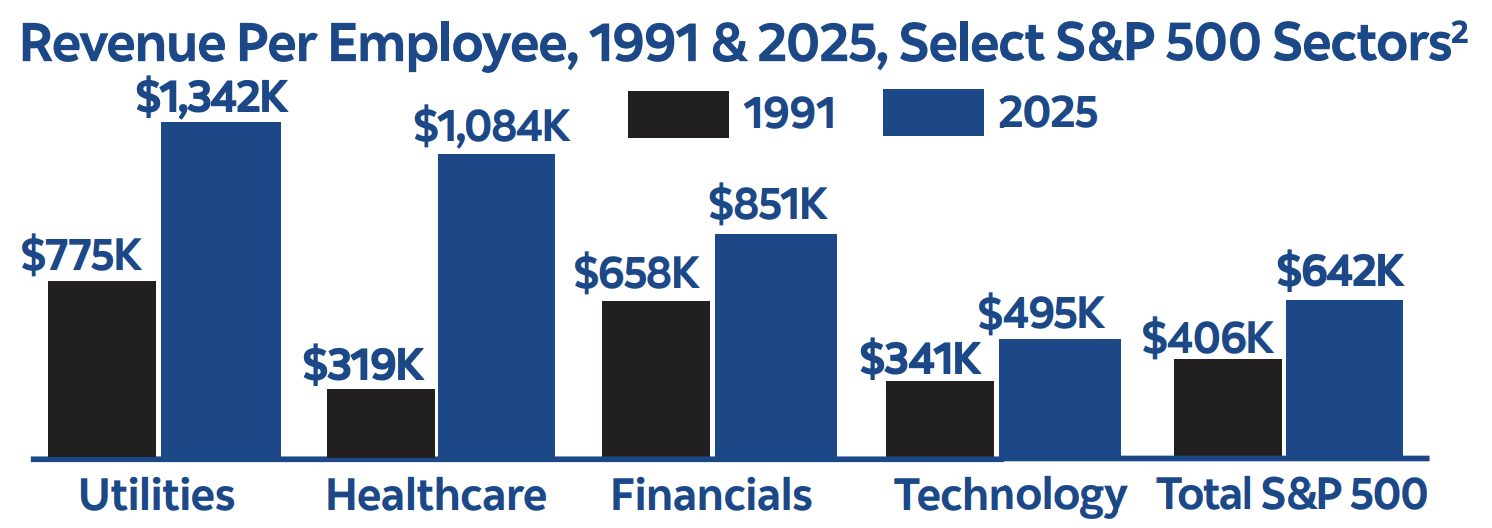

The current enthusiasm reflects AI’s potential to boost efficiency and productivity across industries. History shows how transformative technology can be: over the past 35 years, advances in computing, the internet, mobile devices, apps and software have driven productivity gains. The chart below compares revenue per employee for select sectors in 1991 and today (inflation-adjusted). AI is also viewed as a platform for innovation. Unlike earlier technologies that improved efficiency in isolated areas, AI is enabling new ways to create, design and drive advances across many sectors.

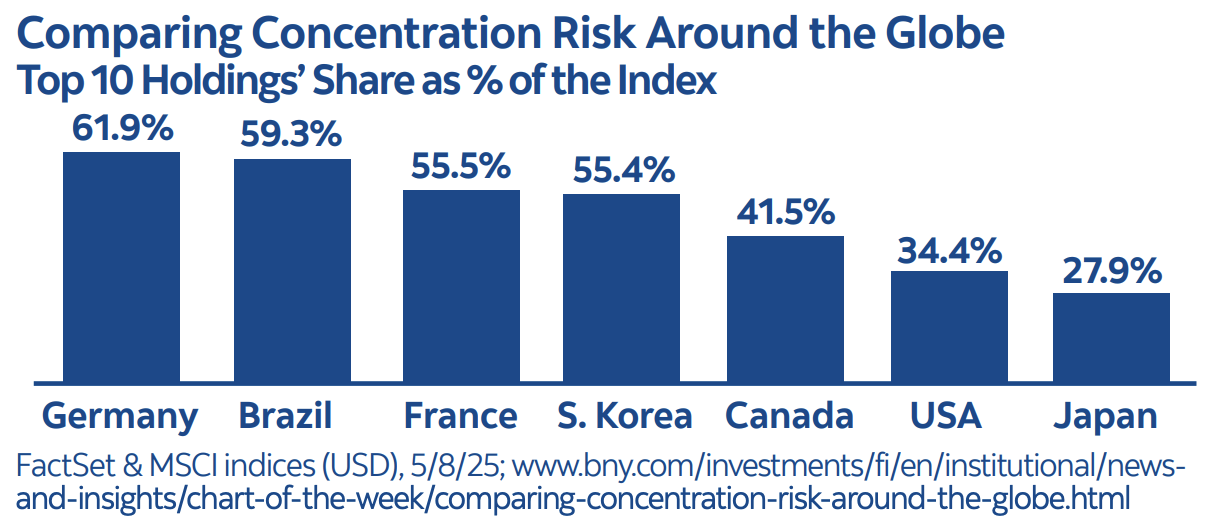

While the mega-tech firms now account for more than one-third of total S&P 500 market capitalization, this concentration has left some investors nervous. Yet, equity market concentration is not unusual; it’s been a recurring feature throughout time. Globally, the largest companies command a significant share of the index, and the U.S. is no exception. In fact, markets worldwide—including Canada—show an even higher concentration of top 10 holdings than the U.S.

Some have compared the current tech rally to the dot-com bubble of the late 1990s. However, it’s worth remembering that today’s large tech firms are very different from the internet darlings of that era. They continue to deliver substantial earnings growth, generate significant cash flow and are well diversified, having acquired more than 800 companies while expanding across multiple industries. In many ways, they function as modern conglomerates of advanced technology—growing organically but supported by multiple engines of innovation.

As Bloomberg suggested: “They go by the Magnificent Seven, but act more like the Magnificent Seventy. Viewed this way, as dozens of companies within each, concerns about their record weighting in the S&P 500 miss the point: the index may still be as diversified as ever.”3

What does this mean for equity markets going forward? Taken together, the investment, innovation potential and diversification of today’s mega-caps may help put into perspective their elevated concentration—and the investor enthusiasm they continue to attract.

1. https://www.reuters.com/business/finance/buybacks-take-backseat-ai-drivesrecord-us-capex-spending-2025-10-27/; 2. https://ritholtz.com/2025/08/themagnificent-493/; 3. https://blinks.bloomberg.com/news/stories/T0MDB8GQ1YPV

.png)

.png)