.png)

.jpg)

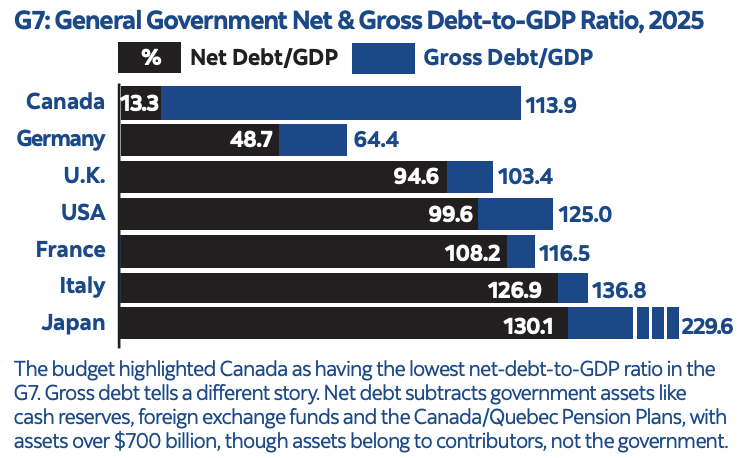

Delivered in November instead of the spring, this year’s federal budget, described as “generational,” projects a $78.3 billion deficit in 2025-26, falling to $57.9 billion by 2028-29, and adding $322 billion of debt over the period. The increase comes from $450 billion in new spending, directed toward infrastructure, competitiveness and defense. Public debt charges are expected to rise by $22.7 billion. By 2030, Canada will spend an estimated $1.46 billion per week on interest payments.1

No changes were made to federal personal or corporate tax rates. The budget confirms the middle-class tax cut, reducing the lowest personal income tax rate from 15 percent to 14.5 percent in 2025, and 14 percent thereafter. Here are notable proposed personal income tax measures:

• Top-Up Tax Credit. This effectively maintains the 15 percent rate for non-refundable tax credits claimed on amounts in excess of the first tax bracket threshold to prevent taxpayers from facing higher tax liability under the lower bracket rate for 2025 to 2030 tax years.

• Personal Support Worker (PSW) Tax Credit. Introduces a temporary five-year refundable tax credit for eligible PSWs working in approved facilities equal to 5 percent of eligible earnings, up to $1,100 annually (excluding workers in BC, NWT, NFLD due to existing agreements).

• Trusts & 21-Year Rule. Broadens anti-avoidance provisions for certain transactions involving trusts that aim to sidestep the 21-year deemed disposition rules.

• Bare Trust Reporting Deferral. Defers bare trust reporting requirements to taxation years ending after December 30, 2026.

• Canadian Entrepreneurs’ Incentive: Cancelled. Confirms that this incentive, announced as part of Budget 2024, will not proceed.

• Luxury Tax Changes. Eliminates the luxury tax on aircraft and boats after November 4, 2025, but retains the tax on automobiles.

• Underused Housing Tax: Repealed. Effective calendar year 2025.

• Registered Plans: Small Business Investments. Starting in 2027, extends certain investments in specified small businesses to RDSPs; investments in shares of eligible corporations and interests in small business investment limited partnerships/investment trusts will no longer be qualified investments for registered plans.

1. https://financialpost.com/news/good-bad-and-ugly-canada-budget-2025 Please note: At the time of writing, these measures have not been enacted into law

.png)

.png)