.png)

Amid equity market enthusiasm and rising P/E ratios, stock valuations are back in the spotlight. Given elevated equity market valuations, we’re increasingly asked: Do valuations still matter?

There are many ways to value a company or stock, but there are two main categories: absolute and relative valuation.

- Absolute valuation quantifies a company’s intrinsic value based on fundamentals such as cash flows or growth. A widely used model is the discounted cash flow (DCF) analysis.

- Relative valuation compares a company to others in its peer group, typically using financial ratios. Most notably, the price-to- earnings (P/E) ratio compares share price to earnings per share.

A Closer Look at Today’s Valuations

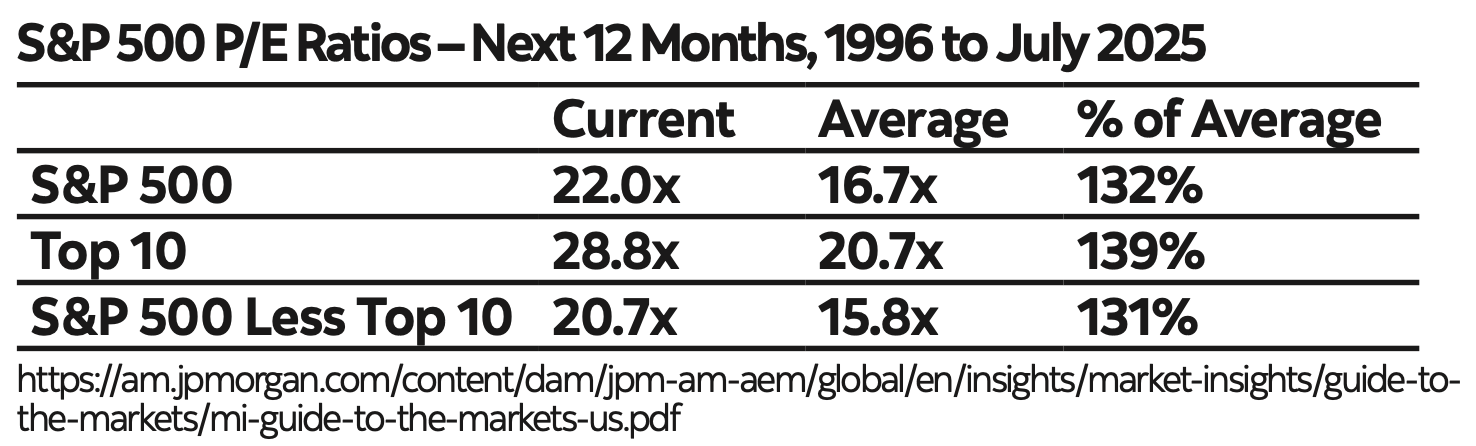

Where do markets stand today? At the end of June, the forward- looking P/E ratio for the S&P/TSX Index was 17.0x.1 For the S&P 500, it was around 22.0x, with the top 10 stocks in the index at 28.8x—both significantly above long-term averages:

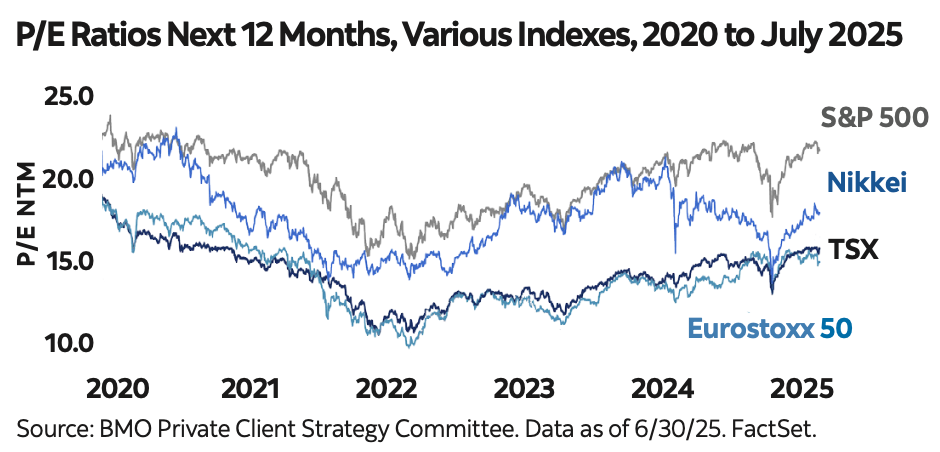

When compared to other markets, Canada’s index typically trades at a lower valuation than the S&P 500 (top graph). This reflects a greater concentration in value-oriented sectors like energy and financials, versus the larger growth-sector weightings in the U.S.

To understand why valuations are elevated, it helps to consider the factors that drive stock prices. The price of any security reflects what investors are willing to pay, influenced by both fundamentals and sentiment. Several factors may help explain elevated valuations today:

- Lower interest rates — When future cash flows are discounted at a lower rate, their present value increases.

- Earnings expectations — Higher anticipated profit growth can support higher valuations.

- Growth leadership — High-growth sectors, particularly big tech, often justify elevated multiples if strong returns, innovation and productivity gains are expected to persist.

- Market sentiment — Periods of optimism (and euphoria) can push prices well above historical norms, exceeding intrinsic value. Conversely, when the dominant emotion is fear, prices often fall short of value.

“Price is What You Pay; Value is What You Get”2

While markets can occasionally outpace or fall behind fundamentals, history shows a strong long-term relationship between stock prices and corporate earnings.3 Over time, fundamentals such as earnings growth, profit margins and return on capital tend to reassert themselves—even when short-term dislocations occur. Elevated valuations can limit upside potential if prices already reflect optimistic future outcomes, and amplify downside risk if expectations aren’t met or macro conditions worsen.

The price you pay remains important to achieving strong long- term outcomes. Valuations still matter: while they cannot predict short-term market movements, they remain a reliable compass for investors, guiding decisions that balance opportunity with risk.

1. Projected, as of July 31, 2025, S&P Global; 2. Attributed to Warren Buffett; 3. See Exhibit 119, Page 179: https://privatewealth.goldmansachs.com/outlook/2025-isg-outlook.pdf

.png)

.png)