.png)

Growing economic uncertainty, rising geopolitical risk and persistent trade and policy tensions are driving a shift toward more defensive positioning across markets. This comes against a backdrop of historically elevated equity valuations following a multi-year run, while returns from bonds and money-market funds remain subdued.

Gold and Silver: A Debasement Hedge

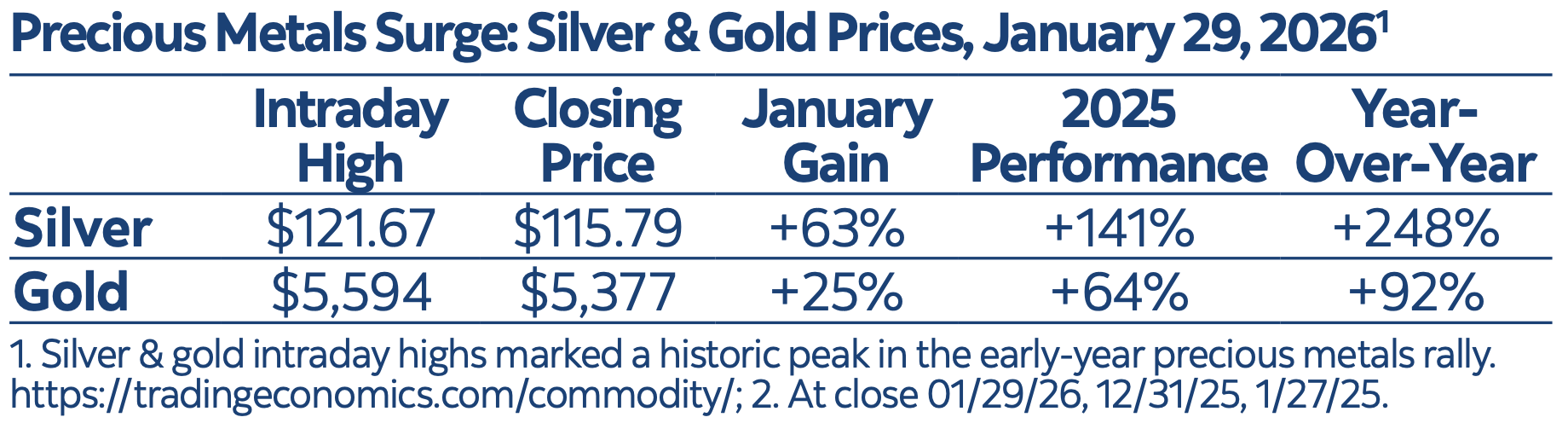

The start of 2026 has been remarkable, though volatile, for gold and silver. In January, gold reached an intraday high of almost $5,600, marking a rise of over 92 percent year over year. Gold futures posted the largest single-day dollar gain on record, rising by about $231 per ounce, before sharply correcting in early February. Silver, long considered undervalued due to the dominance of paper contracts over physical bullion, also saw its biggest one-day percentage move in about 45 years, with a jump of more than 5 percent. By the end of January, silver had surged to around $120 per ounce, up 63 percent in the month of January alone, and over 248 percent year over year. It, too, fell significantly from its record highs at the start of February.

Some attribute this to the “debasement trade”: an effort to preserve purchasing power amid monetary expansion and fiscal overreach. The investment thesis is simple: when governments expand the money supply aggressively, keep interest rates below inflation or run large fiscal deficits, the real value of cash and fixed-income assets erodes. Recent developments have reinforced this concern. In Japan, yields on long-term government debt surged to record levels after the government unveiled a plan to increase spending and cut the consumption tax in January. Those worried about weakening currencies are increasingly turning to gold and silver as stores of value, as precious metals represent a defensive, tangible asset class.

Deglobalization and the Commodities Imperative

At the same time, trade wars, tariffs and geopolitical tensions are also reshaping capital flows and reserve strategies. The broader trend of deglobalization, with nations prioritizing self-sufficiency and national security over international interdependence, is driving demand for precious metals and other real assets. Since 2022, central banks in countries like Poland, Turkey, India, China and Kazakhstan have markedly increased gold reserves, partly in response to geopolitical tensions or threats of sanctions. This has raised the question: Could a commodities supercycle be underway?

The U.S. Dollar and U.S. Treasuries: Under Pressure

Historically, the U.S. dollar and U.S. Treasuries have been the ultimate safe-haven assets. However, this is changing. The dollar hit a four-year low in January, prompting headlines like “How Trump Is Debasing the Dollar and Eroding U.S. Economic Dominance.” With interest rates at low levels and pressure for further cuts by President Trump, returns on Treasuries may be further losing appeal. Beyond the U.S. dollar, the traditional appeal of other safe-haven currencies is under strain. The Japanese yen, once a classic refuge, has been weakened by inflationary pressures and fiscal stimulus, leaving the Swiss franc as one of the few stable currency alternatives.

What Next?

Is the enthusiasm for these defensive trades overextended? Indeed, gold and silver’s gains to start the year were stretched by historical standards. That said, maintaining diversified exposure to defensive sectors, including commodities, other alternative investments and resilient segments of the equity market, can help protect against inflation, currency debasement and geopolitical shocks. This may be especially relevant given that, for at least the next 2.5 years, the global landscape is likely to experience continued unravelling of the post- Cold War economic and political order.

.png)

.png)