.png)

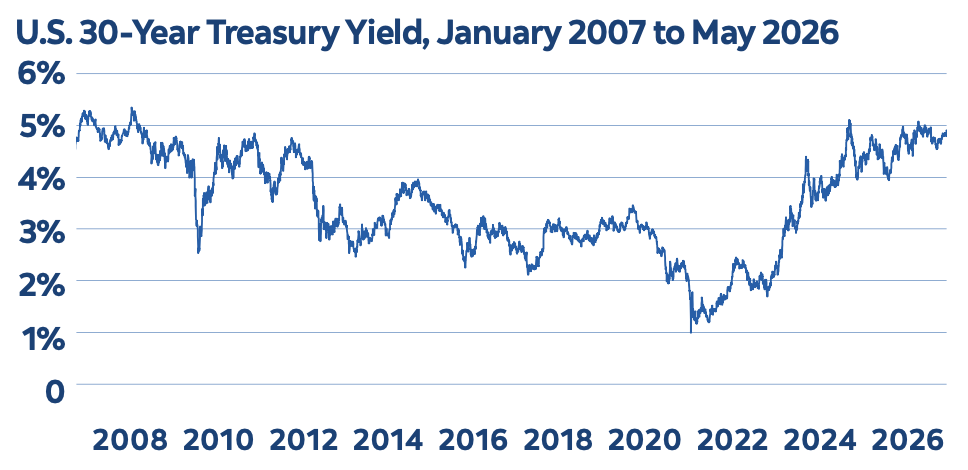

In the spring, bond yields rose to levels not seen in decades. The 30-year U.S. Treasury yield reached its highest point since before the Great Financial Crisis of 2008 (chart). Japanese long-term bond yields hit their highest levels this century. Canadian government bond yields also climbed to multi-year highs.

What prompted these moves? One factor is growing concern over government debt levels, which continue to rise with limited signs of stabilization. To finance persistent deficits, governments must issue more bonds. This is particularly notable in the U.S., where elevated defence spending has added to existing fiscal pressures. Japan’s debt burden has also risen substantially due to sustained government spending, reaching roughly 248 percent of GDP, the highest globally by this measure.1 Others point to persistent inflation pressures, reinforced by elevated oil prices from the Middle East conflict.

Together, these factors contributed to a global bond market sell-off in the spring, pushing yields higher. Since the value of a bond at maturity is fixed at issuance, higher inflation reduces the real value of those future payments, making existing bonds less attractive. In addition, elevated fiscal risk can increase the risk premium demanded by investors for holding long-duration government debt. Because bonds trade in secondary markets, falling prices translate into higher yields. As a result, when governments issue new bonds, they must offer higher returns, which pushes yields up across the curve.

Are rising rates a cause for concern? Higher long-term yields have historically weighed on equities through higher discount rates, though that relationship has been less consistent in recent years. So far, equity markets have largely shrugged off the bond market repricing.

One interpretation is that this reflects a gradual normalization of yields rather than a purely restrictive signal. For several years, the yield curve was inverted, meaning short-term rates were higher than long-term rates. Under more typical conditions, long-term yields should be higher than short-term yields to compensate investors

for the longer holding period. It is also worth noting that the 30-year U.S. Treasury yield has averaged around 6.2 percent over the past 50 years. By the end of May, it stood near 5.1 percent, still below long- term historical norms.

However, higher yields are feeding through into consumer lending rates. The U.S. 30-year fixed mortgage rate, a key barometer for housing finance, recently surpassed 6.5 percent. In Canada, the five- year government bond yield, which forms the basis for five-year fixed- rate mortgages, rose above 3.3 percent, its highest level since July 2024. This may weigh further on already weakening housing activity.

Complicating matters, elevated inflation has reinforced expectations that central banks may need to keep rates higher for longer, or tighten further. This marks a contrast to earlier in the year, when inflation appeared to be moderating, and markets had largely priced in rate cuts. It also comes after a prolonged period of substantial fiscal and monetary stimulus, which has eroded purchasing power and widened wealth disparities. Higher interest rates also increase government debt servicing costs, compounding fiscal pressures over time.

What should investors do? For investors looking for exposure to assets that are more resilient in a higher-rate environment, there may be considerations within a diversified portfolio. This includes real assets, businesses with pricing power and companies that generate stable cash flows that are less sensitive to inflation volatility. By contrast, segments of the market reliant on low discount rates, such as high-growth equities, long-duration assets and highly leveraged businesses, tend to be more exposed when yields remain elevated. For now, however, higher bond yields may not necessarily offer a clear signal about the broader economic or market outlook.

1. https://tradingeconomics.com/japan/government-debt-to-gdp

.png)

.png)